ISSN: 1204-5357

ISSN: 1204-5357

Hanudin Amin, Mohamad Rizal Abdul Hamid, Geoffrey Harvey Tanakinjal & Suddin Lada. Universiti Malaysia Sabah, Labuan International Campus, School of International Business and Finance, P.O. Box 80594, 87015, F.T. Labuan, Malaysia.

Web: http://wwwkal.ums.edu.my

Email: hanudin_zu@yahoo.com;

Email: ejalrizal@yahoo.co.uk;and

Email: tanakinjal@yahoo.com;

Email: suddin@mailkal.ums.edu.my

Visit for more related articles at Journal of Internet Banking and Commerce

This study analyzed the undergraduate students' willingness on adopting the usage of mobile phone in banking transaction' focusing on Islamic banking in FT, Labuan. Research has been conducted to analyze the students' attitudes and expectations toward mobile banking. Furthermore, students' socio-demographic elements were also studied and analyzes in relations with the study. As noted, sample was taken from students of Universiti Malaysia Sabah, Labuan International Campus. A total of 615 students were approached using convenience sampling modes. And, the finding illustrate that students tend to learn and adopt mobile banking in their banking transactions. In addition, the results also demonstrate students' attitudes and expectations to be the most consistent explanatory factors in predicting their willingness on adopting mobile banking usage in the future. In the nutshell, the findings were in-line with the previous study conducted by Howcroft, Hamilton and Hewer (2002), Sivanand, Geeta and Suleep (2004) and Laforet and Li (2005).

There is a growing number of literature concerning to "mobile banking" service with aims to understand the attitude of the respondents over mobile banking (for example, Karjaluoto, Koivumaki, and Salo, 2002; Howcroft et al., 2002; Mattila, 2003; Sivanand et al., 2004; Laforet and Li ,2005; Riivari, 2005; and Wan, Luk and Chow, 2005). However, these studies are targeted on the general population as respondents for their study sample, although some have previously using sample of specific segments. The study conducted by Laforet and Li (2005) using sample of general respondents from six major cities of China, including Beijing. Sivanand et al. (2004) used sample of public population from Klang Valley in Peninsular Malaysia and Howcroft et al. (2002) used sample of young and employed respondents from the United Kingdom.

Mobile banking is defined as the newest channel in electronic banking to provide a convenience way of performing banking transaction which is known as "pocket-banking". Kohli (2004) claimed that the mobile banking service gives customers the convenience of account access information and real-time transaction capabilities. Hamzah (2005) said that "mobile banking" brings convenience and enhanced value. Riivari (2005) claimed that the opportunity for mobile services is three times as many mobile phone users as those who use online PCs and they are now ready for anywhere, anytime applications that match their lifestyles. A mobile phone was considered as a necessity rather than communication tool (Samad, 2004) which purportedly would significantly affect to the application of mobile banking in Islamic banks. Currently, only one Islamic bank has been aggressively offering mobile banking in Malaysia--namely Bank Islam Malaysia Berhad (BIMB) via its database (bankislam.SMS). Other fullfledged Islamic banks such as Bank Muamalat Malaysia Berhad (BMMB) and RHB Islamic Bank plan to offer mobile banking service in the near future. From the conventional side, Hong Leong Bank (HLB) is the first conventional bank to offers mobile banking for their customers (1) SMS banking and (2) mobile credit card. Choosing mobile banking as part of the study analysis is due to two (2) particular reasons. First, the popularity of mobile phone is due to increase over time because of its flexibility for communication purposes. Second, mobile banking helps to reduce the transaction cost more valueadded for the customers.

Considerable attention by many researchers on mobile banking has motivated the researchers to further enhance the study on "mobile banking" but more narrowed towards university students' perspective. University students are defined as undergraduate or someone from the aged of 20-30 years old who also used a mobile phone either using a leased-line or prepaid services and also had previously open an account with one any banks in Malaysia. For the purpose of this study's students' of Universiti Malaysia Sabah-Labuan International Campus were taken as study sample. University students' were chosen based on two (2) criteria. First, university students in general constitute a sizeable market segment of the Malaysia banking industry perhaps to optimistic in nature, all of them have already either acquired an account or have a basic knowledge about basic banking transaction (especially matters concerning their education loans). Second, there is a tendency for every university students to acquire a mobile phone, due to its necessity concern, thereby creating a new room of applying mobile phone as a banking channel.

Noteworthy, mobile phone are no longer justified to its traditional usage/functions: (1) voice conversation, and (2) SMS (Short Message Services). Nowadays, the mobile phones even facilitate for a real time teleconference through 3G (Third Generations). Nonetheless, from the banking perspective, mobile phones introduce a new channel of distribution for the banking industry?and the demand are keep on increasing?hence entrenched its feasibility as a new medium of banking transaction.

The present study is conducted in order to investigate the attitudes and expectations toward mobile banking in Islamic banks by using a sample of university students. The student's attitudes are important in order to justify their adoption for mobile banking in the future. The student's expectations are important to analyze what supposedly they want from Islamic banking product offerings. The study also investigates either the university's students are homogeneous or heterogeneous about their responses in this study. This can be further investigated by the five (5) null hypotheses. Hypothesis 1: There is no significant relationship between the mobile banking perceptions exhibited by race groups. Hypothesis 2: There is no significant relationship between the banking selection criteria exhibited by Muslim and non- Muslim students. Hypothesis 3: There is no significant relationship between the mobile banking perceptions exhibited by age groups; Hypothesis 4: There is no significant relationship between the mobile banking perceptions exhibited by Male and Female students. Hypothesis 5: There is no significant relationship between the mobile banking perceptions exhibited by Labuan School of International Business and Finance (SPKAL) and Labuan School of Informatics Science (SSIL) students.

A survey conducted by Wan et al. (2005) found that demographic backgrounds were strongly associated with adoption of all banking channels except ATM (Auto-teller Machine). Another finding revealed that males were slightly more likely to adopt internet banking than their counterpart-- female. In addition, the adoption of Internet banking was identified to be highest among the middle adulthood, but lower for younger or older customers. Whereby, telephone banking was not highly adopted by all age groups but was used more frequently by customers in their middle or mature adulthood.

Riivari (2005) research on mobile banking based on qualitative approach found that mobile banking is accelerating fast around Europe. Another argument supporting the statement revealing that mobile banking in particular has finally become a fast, user-friendly and affordable service. Customers are now used to mobile applications and are actively using services that help them in their increasingly mobile lifestyles. This lifestyles is synonym with young users.

Laforet and Li (2005) research on mobile and Internet banking claimed that the younger consumers were more interested in online and mobile banking topic than older consumers. However the respondents? level of education was not found to influence online and mobile banking adoption in China. In addition, at least among the urban population surveyed, 33 per cent used online banking and 14 per cent used mobile banking. Thus, the level of awareness of such services was low in China.

Sivanand et al. (2004) research on mobile internet banking in Klang Valley of West Malaysia found that almost all respondents (92.7 per cent) are familiar with Internet usage. However, it further indicates that only 9.6 per cent are currently using the mobile Internet banking services. Meanwhile, only 30.4 per cent have intentions to adopt mobile Internet banking services readily. Another finding indicated that ease of access is one of the important factors in mobile banking adoption which is significant at 0.05.

According to study reported by Malaysian Communications and Multimedia Commission (MCMC) in 2004 as cited in Samad (2004), indicated that younger user equal to 12.3 per cent of the total utilization, which is beyond the respondents, aged 50 (9 per cent). "Younger users" for this study means teenagers (aged 15-25), consisting of secondary students and university students. Another important finding revealed that Malay teenagers were higher user among the other races comprising of 47.50 per cent compared to Chinese (32.4 per cent), Indian (6.9 per cent) and other bumiputra (5.4 per cent).

A study conducted by Mattila (2003) discovered that: (1)-pay bills cheaper, (2)-have faster data transmission rate, (3)-authenticate with mobile phone to internet bank are considered as the main factors for mobile banking adoption. Another finding revealed that gender seemed to have slightly impact on mobile service usage. A user of mobile banking belonged most often to age group 25 to 34 years old, which is the age where the university students graduated and employed thereafter.

A study conducted by Lee, McGoldrick, Keeling and Doherty (2003) discovered that the relative advantage of using 3G mobile banking services would increase one's self-prestige as what intended by young users. Another finding revealed that, the "perception" and "attitude" were the factors for mobile banking adoption. For instance, previous experiences of other mobile phone systems may generalize to beliefs about the ability to use 3G technologies for banking purpose.

A study conducted by Howcroft et al. (2002) revealed that young consumers were more likely to adopt Internet or telephone banking. Younger consumers value the convenience or time saving potential of online and mobile banking more than older consumers. Possibly consumers with lower educational qualifications have less access to the Internet and telephone banking. Howcroft et al. (2002) further found the educational levels of respondents did not affect the use of telephone or online banking.

A study conducted by Karjaluoto et al. (2002) investigated the bank customers' perception about private banking in Finland. The results imply a statistically significant differences (p<0.01) in age t (640) =6.632, education t (635) =-4.094, income t (609) =-5.615 and profession t (75.38) =7.607. Finding also indicated that high frequency users for mobile phone, Internet bank, ATM and others were those aged around 35-49 totaled 281, which were considered as profitable segment for banks.

Al-Ashban et al.'s (2001) study discovered that income levels and education play a vital role for telebanking technology adoption. Findings reveal that customers tend to increase their usage of telebanking services as a function based on their past experience (exposure). Also, young respondents were more interested in expanded banking services (either tele-banking, mobile banking etc). The importance of the telephone based services is highly correlated with the income level, age and education.

In conducting this study, the researchers have chosen university students as a sample of the study. The underlying reasons of choosing students to participate in this research based on three (3) assumptions;

(1)Students have the tendency to learn and adopt an electronic device as a mean of lifestyle and to be looked as trendy;

(2)Students understanding of mobile phone for communication and chatting are narrow down due to mouth-to-mouth informal conversation "viral-communication"; and

(3)Students mostly used mobile phone for voice-communication and SMS to get connected either with their family members, friends, teachers and etc.

Sampling Design

The sampling design that the researchers used is "convenience sampling". The sampling is collected from respondents by the researchers based on the questionnaires distributed. The whole population of students at the university's campus is estimated at 1,938 students. The sample size of respondents chosen to participate for the research is around 615 students and the questionnaire is distributed randomly among the students. By studying the sample, the researchers could depict a conclusion that would generalize the population interest.

Research Instrument

A set of questionnaires was prepared for the survey (totaled 615 sets questionnaires). The questionnaire was distributed to the students at the Universiti Malaysia Sabah-Labuan International Campus. They were chosen through "convenience sampling"; with the intention of generalizing the population and also giving equal chances for each students of being selected for the study. This was ensured the accuracy and precision of the results. The purpose of these questionnaires is identifying feedback and response of the students regarding to the mobile banking service in Islamic banks. The questionnaire is divided into three (3) sections. Section A: to gather the respondent's characteristics. Section B: to gather the respondent's attitudes towards mobile banking based on five-point scale. Section C: to gather the respondent's expectations towards new service and product offered by Islamic banks constructed using liked-scale method.

Data Analysis Technique

The distributing questionnaires was calculated and statistically analyzed by the researchers using SPSS 11.0 technique. A number of descriptive analyses are performed to extract relevant points. In addition, one-way ANOVA analysis is performed to answer the stated hypotheses. Finally the data are organized and presented in a table forms-based on the researchers discretion

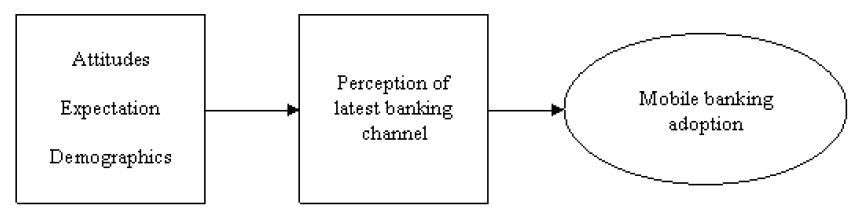

The model

Verification of the data

Based on the reliability analysis, Cronbach's Coefficient Alphas for both measures namely "attitudes" and "expectations" have been calculated by using SPSS 11.0. The alpha value for "attitudes" found to be 0.7444, which concurred with test performed by Sivanand et al. (2004) who found that alpha value to be more than 0.7000. For expectations, the alpha value found to be 0.8764 which is suggested that the analyzed variable were considered to be a good measure for the study. According to Tasir and Abu (2003) who mentioned that the maximum value for reliability test is equal to 1, if the alpha value found to be less than 0.6, thus it may not be a good measure. However, this study showed that both elements have alphas of more than 0.6, therefore, indicating that these elements have good analyzed variables qualifying for further analysis.

Demographics

From Table 1, the proportion of male and female respondents was not in equal proportion for the survey--since it was conducted based on convenience sampling, with 39.8 per cent male and 60.2 per cent female, aged between 20-31 years old (99 per cent) and 26-31 years old (1 per cent only). The researchers found that, there was positive participation from the respondents in rating their priorities of mobile banking. As a result, there were 615 completed answered questionnaires were returned to the researchers, yielding a response rate of 100 per cent. The high response rate as found here was supported by the study conducted by Laforet and Li (2005) who found that younger consumers were willing to participate in the mobile banking survey. Also, the distribution of students both from SPKAL and SSIL was not equal, with 67.3 per cent from SPKAL whereas only 32.7 per cent from SSIL. In terms of religious belief, Islam constituted 57.6 per cent, followed by Christian with 26.2 per cent, Buddhist with 11.1 per cent and the rest equal to 5.2 per cent. These figures were suggesting that Muslim students would contribute more for the sizeable market segment for Islamic banks, whereas Hindus students due to its minuscule population among the campus dwellers--portrayed a lack of participation in this survey. Noteworthy, the change of status, from students to employed individuals may significantly affect the adoption mean for mobile banking in the future.

Table 1

Based on Table 2, the respondents' information about their attitudes over mobile banking is presented. Attitudes of respondents' were analyzed by ten (10) attributes as depicted on Table 2. The results confirmed that the respondents agreed on the basis that mobile phone was a convenience device for communication, with mean of 4.33. In terms of banking purposes, the respondents suggested that Islamic banks need to constantly adopt mobile banking since it offers a comparative advantage to the banks. In sum, most of the respondents opted to adopt the mobile banking in the future as reflected by mean of 4.07. In addition, 29.6 per cent of the respondents claimed that, mobile banking offered cheaper banking transaction compared to conventional banking. According to Mattila (2002) claimed that "pay bill cheaper" would encourage individuals to use mobile banking which was found to be concurred with the present study.

Table 2

Table 3

Table 4

Regardless of the respondents' demographics, the researchers found that the eight (8) variables were essential for Islamic banks to focus on, especially at the product and services Introduction phase. About 66.2 per cent of the respondents claimed to be strongly agreed for the effectiveness of the services to be offered by Islamic banks, with 4.52 mean, ranked at number 1 from the total of 615 respondents. The respondents claimed that they were pleased if Islamic banks can offer an integrated mobile banking to be connected online, in order to offer more flexibility for the services. 61.5 per cent of the respondents supported the variables informally encourages Islamic banks to offer more sophisticated products or services. In the nutshell, majority of the respondents felt that the eight (8) elements as noted here must be given a carefully attention by Islamic banks to adopt into their products offerings policy, perhaps in the future.

Relationship based on Race

The effect of race on adoption of mobile banking in the future was marginally significant, (F.05, 4, 610=20.673), p<0.05 (one-tailed test). As a result, the null hypothesis is rejected. Not all means are equal, so there is a significant difference in the mean number of mobile banking by race groups. In terms of expectations, the same result to be found, significant at 5 per cent alpha, with one- tailed test. This means the respondents have different expectations for mobile banking based on race. Sabahan respondents were likely to give a higher expectation (M=4.58, SD=0.714) than Indian (M=4.00, SD=0.000). In addition, Malay respondents were likely to give a higher expectation (M=4.30, SD=0.639) than Chinese (M=4.11, SD=0.935). Therefore, the null hypothesis is rejected. Expectations of the mobile banking were differed between race groups.

Relationship based on Religion

Attitudes were significantly related to the religion, (F.05, 3, 611=26.239), p<0.05 (one-tailed test). In terms of expectations, the same result was found significant at 5 per cent. Therefore, the null hypothesis is rejected. By rejecting the null hypothesis, concluded the ?attitudes? and ?expectations? of the respondent were different. Meaning, Islamic banks must focus their marketing efforts based on the religion groups need by providing an attractive scheme for different religious beliefs. For instance, Muslims prefer to the marketing program offers a disclosure of right information, reliable and no interestelements. Non-Muslims prefer to the marketing program which is more general and reliable in nature to attract them to use Islamic banking products, such as no discrimination and no Arabic language in brochure.

Relationship based on Age

The effect of age on adoption of mobile banking in the future was slightly significant, (F.05, 1, 613=5.093), p<0.05 (one-tailed test). As a result, the null hypothesis is rejected. Not all means are equal, so there is a significant difference in the mean number of mobile banking by race groups. This result is partially supported by Al-Ashban (2001), who found a relationship between age of the customer and technology adoption. In terms of expectations, because of the small number of respondents in the age group between 26-31 (1 per cent) involved in this study, the effect of age on expectation of new banking product (i.e. mobile banking) was not significantly different p>0.05. Consequently, the null hypothesis is accepted. All means are equal, so for this context Islamic banks must treat different age group, although small in this survey, but it has a deep implication towards the product offerings in Islamic banks.

Relationship based on Gender

The effect of gender on adoption of mobile banking was not found to be significant only at 5 per cent of alpha value, null hypothesis was not rejected. To be more specific, males were slightly more inclined to see mobile phone as a practical way of doing banking business today and in the future (M=4.04, SD=0.754) rather than females (M=3.75, SD=0.851). In terms of adoption for mobile phone as their new device for banking, both gender had similar priority, with (M=4.07, SD=0.685) and (M=4.06, SD=0.799) respectively. This finding is not in line with the work of Howcroft et al. (2002) who found significant difference between gender and telephone-based services and Internet banking. The present finding is also partially not supported by the work of Wan et al. (2005) who found a relationship between gender and technology adoption for banking. Indeed based on Wan et al. (2005), males were likely adopt the electronic banking rather than females which is against the further finding as revealed in the present study, females were likely to adopt mobile banking (part of electronic banking). In terms of expectations, the effect of gender on expectation on how banks develop their products to cater the need of public found to be significant, (F.05, 1, 613=32.662), p<0.05 (one-tailed test), null hypothesis was rejected. To conclude, university students' expectation is different based on gender, for instance females likely to give more attention on matters concerning security (M=4.71, SD=0.552) whereas males give more attention to the effectiveness (M=4.24, SD=0.861).

Relationship based on School

The effect of school types to be attended by respondent on adoption for mobile banking in the future was only slightly different. SSIL students for instance, were likely to adopt mobile banking (M=4.19, SD=0.942) rather than SPKAL students (M=4.00, SD=0.645) at the minimal basis. The null hypothesis is not rejected which means individual were equal although in the practical they can be separated, but statistically there was evidence show they were the same. From the bankers? perspective, this means a little, marketing effort by segmenting these schools under the same package of marketing program would be feasible. However, in terms of expectations, the respondents rigorously wanted Islamic banks to understand their needs. They are different on what they want from Islamic banks, so the banks must cater both groups as different. SPKAL perhaps demand more since they are more knowledgeable on issues of banking rather than their counterparts the SSIL, who have the tendency to ask more since they are better trained in computer mechanism.

The results of this study provide important information for Islamic banks in promoting mobile banking transaction among the university students'. The findings indicated that, the university students' tend to change the way they do banking in the future, more than 80 per cent of the respondents claimed to be willing to adopt mobile banking in the future. These results tend to be supported by Laforet and Li (2005), Howcroft et al. (2002) and Al-Ashban and Burney (2001) who found younger customers were more likely to adopt electronic banking (i.e. mobile banking). These university students' tend to be an active user for mobile banking in the future after been employed as partially supported by Mattila (2003) and Karjaluoto et al. (2002) who found 25 to 34 and 35-49 respectively as active users for mobile banking.

In order to capture the university students as a potential customers for mobile banking in the future, Islamic banks must segregate their customers based on demographic priority (i.e. race, religion, age, gender and field of study). The results of this study imply that the financial providers cannot assume that consumers are homogeneous in terms of their perceptions towards Islamic car financing as being offered by Islamic banks. The attitudes showed to be significant related to race, religion, age and field of study. For expectations--race, religion, gender, and field of study tend to be significant at 0.05. Karjaluoto et al. (2002) found that age to be significant for mobile banking adoption, which is partially, supported the present study result under age groups.

Furthermore, mobile banking is not the only method ensuring the competitiveness of Islamic banks. Nonetheless, it is one of the methods which already a numbers of commercial banks including Islamic banks started to recognize to be effective and applied in banking transaction. Islamic banks must also be pro-active in encouraging university students' to adopt mobile banking service, a simple transaction such as "request an account statement" would be a good starting. To be more recognizable, an active education program would provide a path, especially from the Islamic banks to promote mobile banking services usage among university students'.

Like other studies, this study also has its own limitations. First, this study only employed student as a sample of the study, no further efforts made to explore other user feedback outside the campus area, which may have an affect on the generalization of the results. Other perhaps, because of its geographical implication the research were conducted only in Labuan. Regardless of the limitations, this study has offered an insight into mobile banking in Malaysia as well as to provide a platform for future investigation in terms of mobile banking from a larger sample point of view. Indeed, the results will add to the very limited knowledge presently available about mobile banking study in Malaysia.

Copyright © 2026 Research and Reviews, All Rights Reserved