ISSN: 1204-5357

ISSN: 1204-5357

By Miran Pecenik

Translation by Michele Clara

E-mail: nbctkb@nbctkb.it

URL: http://www.nbctkb.it/

Visit for more related articles at Journal of Internet Banking and Commerce

Pecenik Miran was born in Trieste (Italy), in 1956. From 1978 he worked in the Banca di Credito di Trieste - Trzaska Kreditna Banka, in sectors like Edp and organization. Now he is the chief of Information and Communication Technology (and also Webmaster) in the Nuova Banca di Credito di Trieste - Nova trzaska kreditna banka.

In the last two years he published many articles about the Web on italian and canadian newspapers and his work was mentioned in dozens of articles on financial and Internet magazines, on television and on an italian national teletext. Overall he increased the popularity of the bank with over 700 links all around the world.

He spoke in various meetings, organised by the principal italian banking corporates, such Abi, Ipacri and Istinform. In 1996 worked on a questionnaire of the use of Internet in Italy (nowadays the biggest in Italy, with 1700 answers) and had organised the first italian elections on the Web. In 1997 he tested the push technology with a group of 700 people.

After this exhaustive discussion of the steps that can take an enterprise into electronic commerce, I find it necessary to reflect on what an enterprise might be offering on the Net or, in other words, of the commodities that might be sold on line. Let me try to put forward a list of the enterprises that are currently selling their own products worldwide.

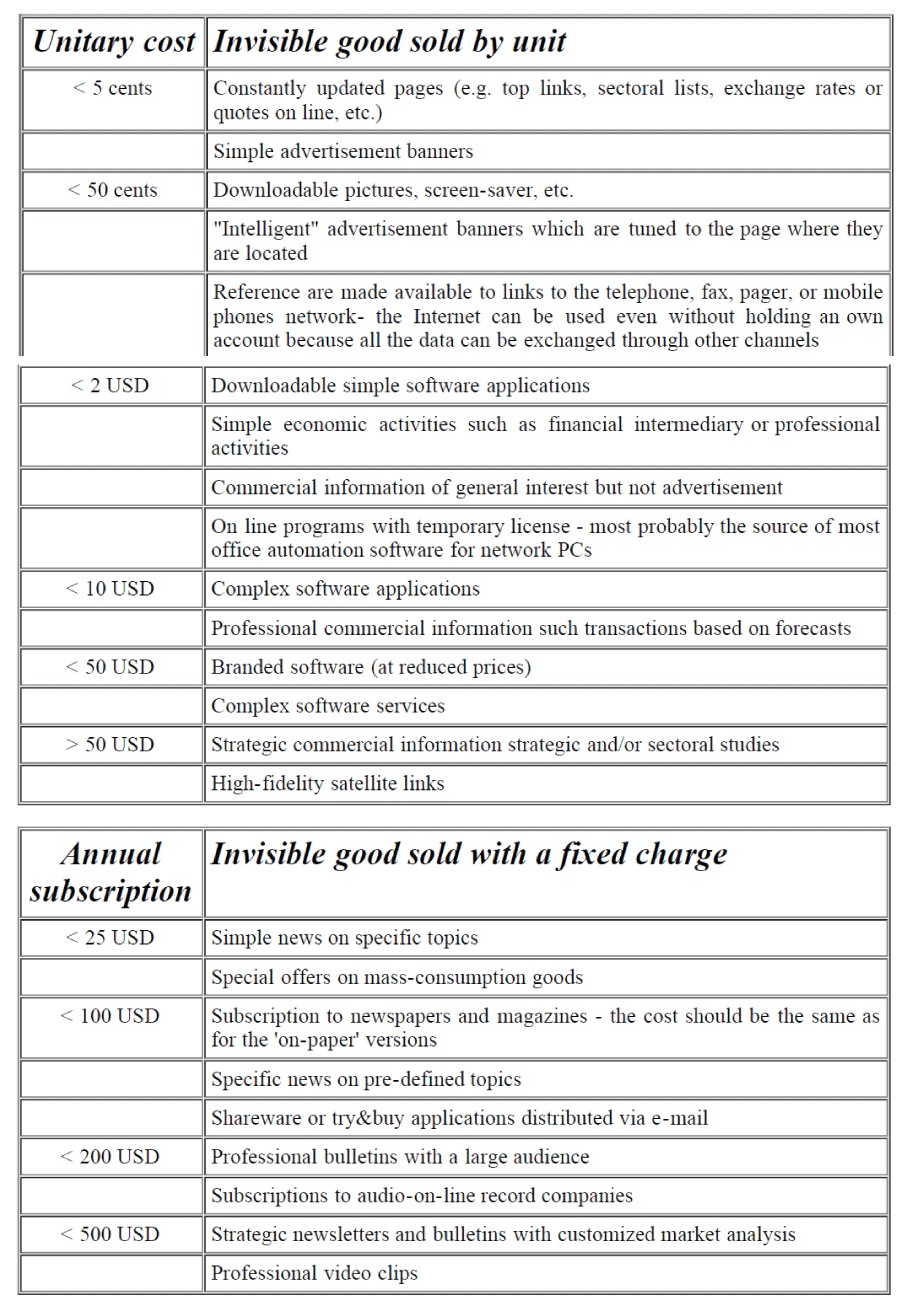

Let me categorize these commodities on the basis of their price and their potential customers. For a start it might be useful to differentiate between 'visible' and 'invisible' commodities. Invisible goods (such as services, software, news, etc.) can be further divided into goods that can be sold by units and those that can be sold with a fixed charge.

In the next two tables we can have a look to a whole range of invisible goods that can be exchanged via electronic transactions.

It should be noted that the transactions involving many of these invisible goods might very well lack any form of control (by the state, the regulators or the consumers associations). It is therefore possible to gain access to the 'deal of the century' or just one of many 'lemons'. The best advice is to try the service for a while to see if it is worth one's money before paying for a subscription.

As it can be easily seen, the list (which is by no means exhaustive and should be read as only suggestive of the countless opportunities available) includes, beside the by now common pages of 'useful links', also the opportunity to download files such as audio or video files and images of all types.

The method of payment for these transactions should also be discussed in details. Many suppliers are not yet connected to secure servers supporting encryption. A recent development is the creation of 'Internet billing companies' that provide secure pages and then divert the payments from the final consumers. Clearly these providers have identified the scope for a profitable business much in advance of the banks, which have in general been very skeptical about new forms of payment such as Digicash e Cybercash, to mention but a few.

Let us now discuss the opportunity for electronic commerce of visible goods. For a start it must be acknowledged that not all such goods can be adequately commercialized on the Net. Here are some examples of goods that have been sold successfully through this new medium of communication.

Books can be sold most easily on line. The classic example is that of the virtual megastore Amazon.com which caters for something like one million clients without a single (physical) bookshelf. Numerous attacks have however been waged against this experience, supporting the purchase of books from the (physical) bookstores on the street.

In collaboration with a bookstore in Trieste (Italy), we have tried to study, back in 1996, the opportunity to sell books on line. The cost of shipping the books elsewhere in Italy was found to be about 2.5 USD. It seemed a price that customers should be willing to pay to receive, at home and in a couple of days, a book otherwise impossible to find. In this case, the payment was to be made upon receipt of the book.

The very same kind of payment was envisaged for a (physical) megastore of computers in Florence (Italy). On their Web site it is possible to select the preferred PC configuration in details and to pick up the computer the day after at any of the affiliated shops, paying what had been indicated on the web page, without any extra charge.

Again in Florence, a provider has succeeded in putting on line some twenty among the most famous local artisans, offering to its customers (worldwide) the very same products that can be found on the city streets and delivering them directly at home. The sale of these products is optimized with respect to the status of the artisans' inventories. In this case the cost is not a key variable, what is vital is that the product should arrive on time even in Japan. And it does ... !!

Along the very same principles and relying upon an existing network of delivery points (such as the Pizza Hut outlets or Hard Discount chains), it may be possible to facilitate the distribution on line of standardized commodities (such as pizza) or even of pre-defined baskets of goods.

For sake of completeness a reference should also be made to other successful experiences such as the sale of CDROM disks (Cdnow) which also offers a valuable service in terms of discography search, of software (Buydirect offered by Cnet) with the opportunity of a pre-purchase trial, of flowers (1-800-flowers) a virtual Interflora, of travel packages (Travelocity) and tickets (Ticketmaster).

If an enterprise intends to sell its products on the Net but lacks the necessary technical capabilities, it can easily join a sale point such a cybermall or a netmarket. These virtual commercial outlets can also be organized on a smaller scale or for the needs of a medium-size town, if a sufficiently large number of customers is present. A so-called "local" bank can evidently play a key role to establish such an arrangement, to centralize and therefore facilitate payments, or to provide guarantees for the commodities sold.

New markets would therefore be disclosed to the enterprises participating to this experiment (by now "clients" of the local bank) and the bank would have the opportunity to strengthen the ties with its customers and to increase their profitability.

In the last year, we have been experimenting with electronic commerce both of visible and of invisible goods.

For nine months we moderated a news service (delivered by e-mail) to over 700 people on some forty different topics. The service complemented a questionnaire on the use of the Web in Italy and it was entirely free. From this experience we drew the impression that the best way to deliver news is most often also the simplest one. Nowadays some enterprises are willing to deliver information using always more elaborate techniques (both in terms of graphic and contents), on the assumption that their potential clients possess computers of the latest generation. The so-called 'push technology' channels seem to be still within the reach of a very limited minority of customers; I would suggest the need to rethink this strategy, making use of a more traditional medium like the e-mail, which I believe to be the most valid element of the Internet.

In the summer of 97 we also tried to sell the tickets for a rock concert that took place in Trieste. Through a simple form, the potential buyer had the opportunity to fill in a request which would be then sent and processed as an e-mail. At most within two days, he or she would be then contacted by a freelance delivery-boy, who would take the tickets directly at his or her home and without any extra charge. Given that the service was only open to the inhabitants of the area, the results have been significant.

Numerous contacts have been established with the clients of our bank including bookstores, computer shops, car retailers, tour operators, estate agencies and supermarkets; in general all displayed some sympathy towards electronic commerce, even though there has been no evidence of the keen interest which normally surrounds those projects with a clear business implications and which would have been needed to start a serious program.

What is holding up the take-off of the Net or, in other words, why is electronic commerce standing still? In the USA, 17% of the users (out of an estimated 50 million users of the Net) admit to buy commodities on line with an average monthly expenditure of around 50 USD. In Italy, it was optimistically estimated that 2.5 million people navigated the Net in September 1997. Nevertheless, it has been almost impossible to find out how many of these users are 'professionals' ones and how many rely on temporary, educational or corporate accounts. It is also estimated that, out of eight people who browse the Net, only one pays a subscription fee for this purpose: this is the case of corporate local networks, cyber-cafes or other types of spot accounts such as, for example, mailboxes with temporary passwords.

From these elements it is clear that the expansion of electronic commerce will be a problem. What could stimulate or hinder such an expansion? Let me dwell on this topic from the point of view of the buyer and of the seller.

The enterprise that decides to have its products bought on the Web opens itself to the global market (if and when it gains a sufficient visibility), with all the pros and cons that are involved. It gets contacted by customers that would have never been reached but for the Net. At the same time, however, it can also encounter new types of problems because it becomes accountable for wrong-doings in the purchase of components, because it discloses information to its competitors, or because it can breach the legislation of some foreign country. All in all, the experience should be positive in most of the cases.

For the buyer, there are clear advantages from shopping on the Net but also disadvantages. Discounts might be available to net-buyers. The real advantage of shopping on the Net coincides however with the opportunity to access information on the products required from a variety of competing sources. Here is the other face of electronic trade. Many US firms admit to be present on the Web not so much to sell, but rather to be competitive, to strengthen their communication with customers, to increase the visibility of their brand and to improve the after-sale services they offer to their customers. Why should these firms be in any way interested in exploring new means of communication, when the existing ones are more than enough?

Copyright © 2026 Research and Reviews, All Rights Reserved