ISSN: 1204-5357

ISSN: 1204-5357

Tahir Masood Qureshi, PhD

Assistant Professor, International Islamic University Islamabad, Pakistan

Postal Address: Faculty of Management Sciences International Islamic University Faculty Block-2, Sector H-10, Islamabad, Pakistan

Email: tahirmasood2002@hotmail.com

Tahir Masood is the Assistant Professor in International Islamic University Islamabad, Pakistan. His areas of interest are Human Resource Management and Information Technology.

Muhammad Khaqan Zafar, MBA-IT

Research Associate, Management Sciences Faculty, International Islamic University Islamabad, Pakistan

Postal Address: Faculty of Management Sciences International Islamic University Faculty Block-2, Sector H-10, Islamabad, Pakistan

Muhammad Khaqan Zafar is a student in Faculty of Management Sciences, Department of Technology Management in the International Islamic University, Islamabad. His current research interest is Information Technology.

Muhammad Bashir Khan, PhD

Professor/Consultant, Management Sciences Faculty, International Islamic University Islamabad, Pakistan

Postal Address: Faculty of Management Sciences International Islamic University Faculty Block-2, Sector H-10, Islamabad, Pakistan.

Dr. Muhammad Bashir Khan is professor in Faculty of Management Sciences and his area of interest is Management.

Visit for more related articles at Journal of Internet Banking and Commerce

Technology is affecting the life of every individual in this present age. Online banking is also one of the technologies which are getting recognition around the globe. There are a lot of customers around the world who are accepting this technology very quickly but in growing countries like Pakistan the adoption ratio is very high. There are many banks which are providing these facilities to customers. The basic purpose of this research is to evaluate the customer acceptance of online banking. Almost 50% of the clients shifted from traditional banking to online banking system. The core reason of this transfer is perceived usefulness, security and privacy provided by online banking.

Pakistan, customer acceptance, online banking, perceived usefulness, security and privacy, amount of information, perceived ease of use.

Technological innovations are having significant importance in human general and professional life. This era can safely be attributed as technology revolution. The quick expansion of information technology has imbibed into the lives of millions of people. Rapid technology advancements have introduced major changes in the worldwide economic and business atmosphere. Information technology developments in the banking sector have sped up communication and transactions for clients (Booz et al, 1997). Online banking is also one of the technologies which are fastest growing banking practices nowadays. It is vital to extend this new banking feature to clients for maximizing the advantages for both clients and service providers.

In this study the customer acceptance of online banking in Pakistan is evaluated. As banking is the most progressive industry in recent years therefore it has its own significance. In recent years, growth and turn-around in Pakistan’s banking sector has been amazing and exceptional due to online technology exploited by the banking sector. The financial institutions are using technology to improve services and their customers are also accepting such technologies. The progressive competitive atmosphere in the banking sector has resulted in developing and operating substitute deliverance channels. The most recent deliverance channel to be introduced is electronic or online banking (Daniel, E. 1999). Electronic or online banking is the latest delivery canal to be presented by the retail banks and there is large customer acceptance rate. Bank branches alone are no longer enough to offer services to meet the needs of today’s high demanding and challenging customers (Bradley, L et al, 2003). So online banking does play a very effective role. This technology is very useful in connecting different branches of the same bank or different banks with each other. Adoption of online banking is increasing day by day because by dint of it, they can save their crucial time and accelerate operations to the convenience of both customers and service providers.

Banking sector:

The financial institutions can scarcely be regarded as a form of innovation. Certainly its tradition virtue and recognized ways of doing business have been a source of pleasure to the sector (Bradley, L et al, 2003). There are different types of financial institutions. Generally speaking, financial institutions are ranked by their capitals or assets. According to the categorization structure of “Istward and Holland”, banks with capital less than US $40 billion are measured as small banks; those with more than US $40 billion but less than US $350 billion are regarded as medium-sized banks; and those with more than US $350 billion are large banks (Huang et al, 1990). Over the past few years a healthy investment has been made in the banking sector. As the financial institutions have a great impact on economy of any country. Their performance truly affects the economy of a country. In Pakistan banking is the most prominent growing sector having 40 banks with lot of branches. This sector contributes share in significant gross domestic product (GDP). These financial institutions are offering various types of services besides conventional banking services, such as, business loans, corporate banking, house financing and car leasing facilities. Over the last three years, almost 70% banks have converted to online banking, providing real-time information. Consequently the performance of banking is increasing not only in urban centers but also in rural areas.

Online banking:

Evolution in human culture has been consummated by the development of new technologies. The last few years have witnessed supreme changes throughout the world (Deshmukh S. G et al, 1995). Due to increase in technology usage the banking sector’s performance increases day by day. Online banking is becoming the indispensable part of modern day banking services. It is expected that 60 % of retail banking dealings will be online in ten years' time (Barwise, P. 1997). A financial institution has a lot of customers around the country; therefore they need their bank online so that they can easily access it from anywhere. Pakistan is also not lagging behind in this venture. Resultantly the customers feel ease in certain banking activities. One would imagine that Pakistani banks would not only be proactive to give online banking service but would also persuade consumers to shift to this form of deliverance of banking services.

Customer acceptance:

Banking industry is also one of the influenced industries adopting technologies which are helpful in providing better services to customers. Quality of service is improved by using technological innovations. Online banking is time-saving. About 20% of retail and 30 % of businessmen will use some shape of Internet banking facility within the next five years (Booz et al, 1997). There will be huge acceptance of online banking with the passage of time with growing awareness and education. A great many people are shifting to online banking and are readily accepting the usefulness of this bounty. Online banking service allows customers to manage their accounts from any place at any time for minimum cost; it gives abundant compensation to the client in terms of price and ease (Ekin et al, 2001). It is a fast growing phenomenon among general public in Pakistan as well. Many factors are attracting the public like ease of use, perceived usefulness, security and privacy. Perceived usefulness is defined as the degree to which a person believes that using a particular technology would improve job performance while perceived ease of use is the degree to which using IT is free of effort for the user (Davis et al., 1989).

Purpose of the Research Study:

The key intention of this paper is to evaluate those factors that manipulate the nature of customers towards online banking and their growing tendency towards the online financial institutions. Therefore main objective of the study is to find out

• Correlation amongst variables and impact of customer acceptance on online banking.

Research Design:

In this research effort “Convenience Sampling” has been used. This method is used to make research procedure faster by obtaining a large number of accomplished questionnaires rapidly and efficiently. The platform which helped us to choose the banking sector is the website of State Bank of Pakistan. This website provides all essential information of the online banking.

Management science research studies have used abovementioned mail, interview and telephone etc. survey methods of information gathering. We followed the similar approach as secondary data in this field is not available in Pakistan. Due to the lack of time and inadequate budget, we primarily used mail survey for data gathering. Through this method we collected a good number of responses from the people of different backgrounds, but few problems condensed the response rate efficacy e.g. some people from village areas are not so much educated, therefore the data collection was slow. To deal with this challenge, one to one interviewing method was started, as a result response rate was getting quicker with high quality, but there were other problems as well, like time consumption and traveling. For eliminating too much traveling, telephonic interviewing method was used. This technique was reasonably more fruitful. For the survey, questionnaires designed consisted of 5 likert scale point, 5 for strongly agree, 4 for agree, 3 for neutral, 2 for disagree and 1 for strongly disagree. Many a time, it happened that the customers’ were not clear about the terminologies used in the questionnaire but this matter was solved through detailed explanation and by one to one discussion.

Response Rate:

For solid research work, information concerning online banking and customer acceptance was collected from the customers who were highly connected with services offered by banks. The customers’ were requested to reply to all the questions to the best of their knowledge. Out of 300 questionnaires we got only 235 responded back. Overall response rate was 78%. After data collection, we coded it in Excel 2003. For analysis purpose statistical tools Regression analysis and Correlation were used.

Research Model:

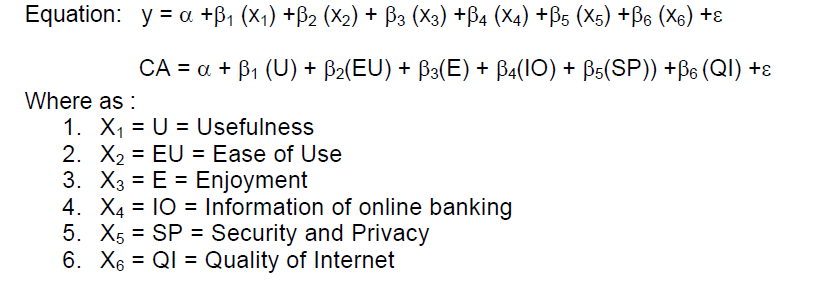

This TMQ Customer Acceptance research model is developed on the basis of previous research studies and variables included are, perceived usefulness, perceived ease of use, perceived enjoyment, the amount of information, security and privacy, internet connection.

Figure 1: TMQ Customer Acceptance of online line Banking model

Equation tested is following:

Hypothesis:

H1. Perceived usefulness (PU) has a positive effect on consumer acceptance of online banking (Davis et al., 1989; Pikkarrainen, T et al, 2004).

H2. Perceived ease of use (PEOU) has a positive effect on consumer acceptance of online banking (Davis et al., 1989; Pikkarrainen T et al, 2004).

H3. Perceived enjoyment (PE) has a positive effect on consumer acceptance of online banking (Davis et al., 1992; Igbaria, M., et al., 1995; Teo et al., 2000; Pikkarrainen T et al, 2004).

H4. The amount of information a consumer has about online banking has a positive effect on consumer acceptance of online banking (Sathye, 1999; Pikkarrainen T et al, 2004).

H5. Security and privacy have a positive effect on consumer acceptance of online banking (Charles et al, 1998; Sathye, 1999; Hamlet et al, 2000; Tan et al, 2002; Black et al., 2002; Giglio, V., 2002; Howcroft, B,. et al., 2002; Pikkarrainen T et al, 2004).

H6. The quality of the Internet connection has a positive effect on consumer acceptance of online banking (Sathye, 1999; Pikkarainen T et al, 2004).

For finding the strength of the relationship between several variables, “Pearson Product Moment Correlation Co-efficient” is used. In this tool, both the variables are treated symmetrically, i.e. there is no peculiarity between dependent and independent variables. Two variables are said to be correlated if they tend to at the same time vary in same direction. If both the variables tend to increase or decrease together, the correlation is said to be direct or positive. When one variable tends to increase and the other variable tends to decrease, the correlation is said to be negative or inverse.

Table 1 is showing correlations for all the variables and Table 2 is signifying descriptive statistics which cover values of standard deviations, means and median. There is a high correlation amongst the independent and dependent variables. Especially between Perceived Usefulness and Customer Acceptance, correlation is (0.75). Mean of the Perceived Usefulness is (4.73), whereas standard deviation is (0.65). This means that the perceived usefulness played a vital role in customer acceptance of online banking. Correlation (0.64) between Security and Privacy and Customer Acceptance is also very high which points out that Security and Privacy is also playing a very critical role in Customer Acceptance of online banking in Pakistan. Mean of the Security and Privacy is (4.05), whereas standard deviation is (0.58). Amount of Information with Customer Acceptance of online banking is showing (0.53) correlation, means the Amount of Information is also very important in acceptance of online banking in customers. The mean and standard deviation is (3.97) and (0.48) respectively.

Table 1: Correlation of Variables

Table 2: Mean and standard deviation

Correlation between perceived enjoyment and customer acceptance is (0.35) with mean (3.88) and standard deviation (0.37). Coefficient of correlation between Perceived Ease of Use and customer acceptance is (0.29), along with mean (3.70) and standard deviation (0.30). Correlation between internet connection and customer acceptance is (0.18), with mean (3.65) and standard deviation (0.28). Coefficient of correlation between perceived ease of use and perceived usefulness is (0.61), the results show that the ease of use increases usefulness of online banking. Correlation between perceived usefulness and Amount of information is (0.60), which indicates that amount of information also increases usefulness of online banking. Coefficient of correlation between perceived enjoyment and security and privacy is (0.57). The results show that security and privacy provided by online banking system gives entertaining environment to its customers. Correlation between perceived ease of use and security and privacy is (0.52), which shows that perceived ease of use has a high association with security and privacy.

We have computed sample mean, the highest mean of perceived usefulness (4.73) is specifying that it is the main factor which is affecting the customers to accept online banking. But internet connection illustrated the lowest mean (3.65), highlighting that it is not a major contributory factor of customer acceptance of online banking.

For calculating the contribution of independent variable towards dependent variable, we adopted Multiple Regression. Table 3 confers the regression Conclusions. This table shows by increasing 1 unit of perceived usefulness will increase customer acceptance by (0.55) units. It means this variable is having strong impact on customer acceptance. This result is significant at 1%. If 1 unit of security and privacy is increased (0.47) units will be increased of customer acceptance of online banking in Pakistan. It shows this variable is having positive impact on customer acceptance with significant at 2%. Likewise if 1 unit of amount of information is increased (0.43) units of customer acceptance are increased with significance of 2%, showing a positive impact on customer acceptance.

Table 3: Regression

By increasing 1 unit of perceived enjoyment (0.35) of customer acceptance is increased, which means this variable has an impact on customer acceptance of online banking. This result is significant at 3%. If 1 unit of perceived ease of use and 1 unit of internet connection is increased (0.15) and (0.10) will be increased respectively of customer acceptances which have a very small impact on customer acceptance of online banking. This result is significant at 4%. So if perceived usefulness and security and privacy are increased a lot of new customers will be shifted from traditional banking system to online banking system.

Study concludes that majority of customers are accepting online banking culture because of many favorable factors. Analysis concluded that usefulness, security and privacy are the main perusing factors to accept online banking system in Pakistan. The other factor is amount of information which is provided to the customers by different means like advertisement through print and electronic media about online banking is useful in customer acceptance of online banking in Pakistan. These factors have a strong and positive effect on customers to accept online banking system. Online banking system is getting appreciation in different parts of the country due to which almost 50% of the customers shifted from traditional banking system to online banking system. (Guriting and Ndubisi, 2004) concluded that perceived usefulness and perceived ease of use are vital factors of online banking acceptance, but in Pakistan usefulness, security and privacy are the major factors. Lot of customers think that it is not easy to use online banking system and people want their money to be secure. In future further research could be a thorough study on online banking practice in organizations considering age and educational level of the customers, keeping in mind the factors like security and privacy of the customers and usefulness of the online banking managers can make decisions regarding market expansion and increasing customers.

Copyright © 2026 Research and Reviews, All Rights Reserved